Markets are underpricing the supply shock stemming from the interruption of oil flows through the Strait of Hormuz. Rates are too low, equities too high and the dollar not strong enough relative to the move in commodities.

The disruption has pushed most commodity prices significantly higher, and a quick resolution looks unlikely. What markets are conditioned to treat as a temporary geopolitical event has already turned into a genuine supply shock.

{kind=link}

Episodes like these are inherently stagflationary: they lift headline inflation while simultaneously weighing on demand, as households spend more on necessities like heating and less on discretionary goods.

That’s a toxic combination for markets, increasing the likelihood that bonds and equities sell off together. For equities, it means higher input costs and less ability to pass those costs on, resulting in margin compression.

This is compounded by rising yields driven by inflation and a corresponding hawkish shift from central banks. A stronger dollar further amplifies the impact, particularly for energy importers and emerging markets.

{kind=link}

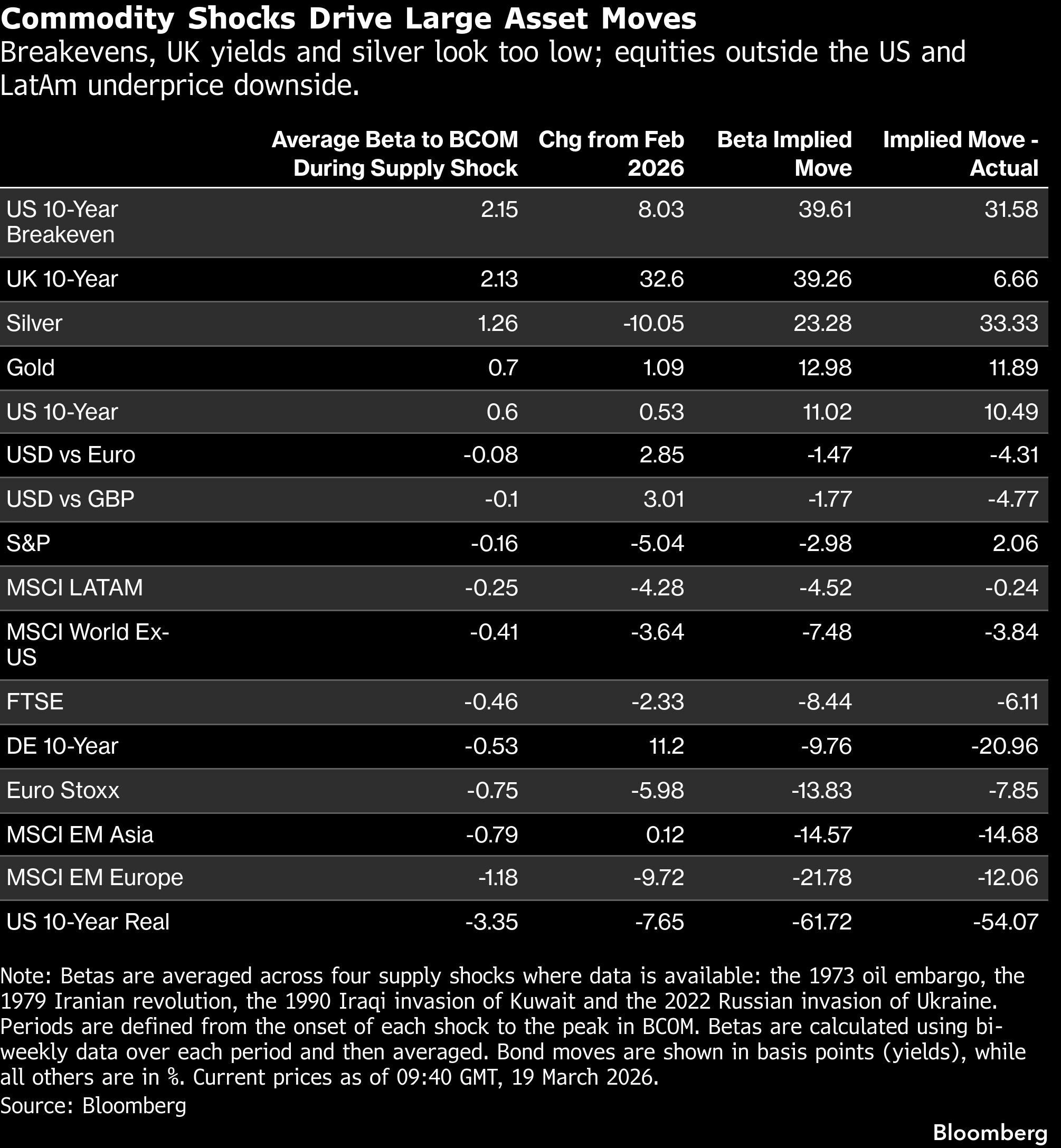

To gauge expected market moves from the conflict in Iran, I looked at the relationship between asset prices and commodities across four previous commodity supply shocks.

Based on the current move in the Bloomberg Commodity Index, those betas imply significantly larger adjustments than are currently priced.

{kind=link}

The gaps are sizable across a number of assets. US breakevens, UK yields and precious metals appear too low relative to the move in BCOM.

Equities in most regions outside the US and Latin America look insufficiently priced for downside, with the greatest vulnerability in emerging markets.

Those regional differences reflect the fact that Asian and European economies are predominantly energy importers, while the US and Latin America are exporters.

There are of course structural differences to earlier episodes. Most notably, the US became a net energy exporter in 2019, flipping the dollar’s relationship with commodity prices.

The dollar now benefits both from haven demand and improved terms of trade (the average beta shown in the table, however, is overwhelmed by the earliest three episodes when the US was an energy importer, resulting in negative beta).

Looking more directly at the Russia–Ukraine shock, Brent rose roughly 32% from the invasion to its peak more than three months later.

The Bloomberg Dollar Spot Index initially lagged as markets assessed the economic impact, but ultimately peaked 15% higher a couple of months later. This time, Brent crude has risen about 56% since the start of the war, but the broad dollar is up just more than 2%.

Regional exposure also matters. In 2022, European equities showed the greatest sensitivity to higher energy prices due to their direct dependence on Russia, while in 1990 the impact was more pronounced in Asia. Today, with Asia more reliant on commodity flows through the Strait of Hormuz, downside risks there appear greater.

In rates, US 10-year yields rose in all four episodes, although the beta varied considerably. Available data suggest breakevens tend to rise sharply with inflation, while real yields reflect a balance between weaker growth and tighter policy expectations.

Policy responses reinforce the point. In none of these episodes did the Federal Reserve cut rates; in three cases it hiked, and in 1990 it paused despite being in an easing cycle.

Fiscal policy could provide some near-term support to growth and equities, but with most developed economies already under deficit strain, this is likely to come alongside higher yields, limiting any positive impact on risk assets.

{kind=link}

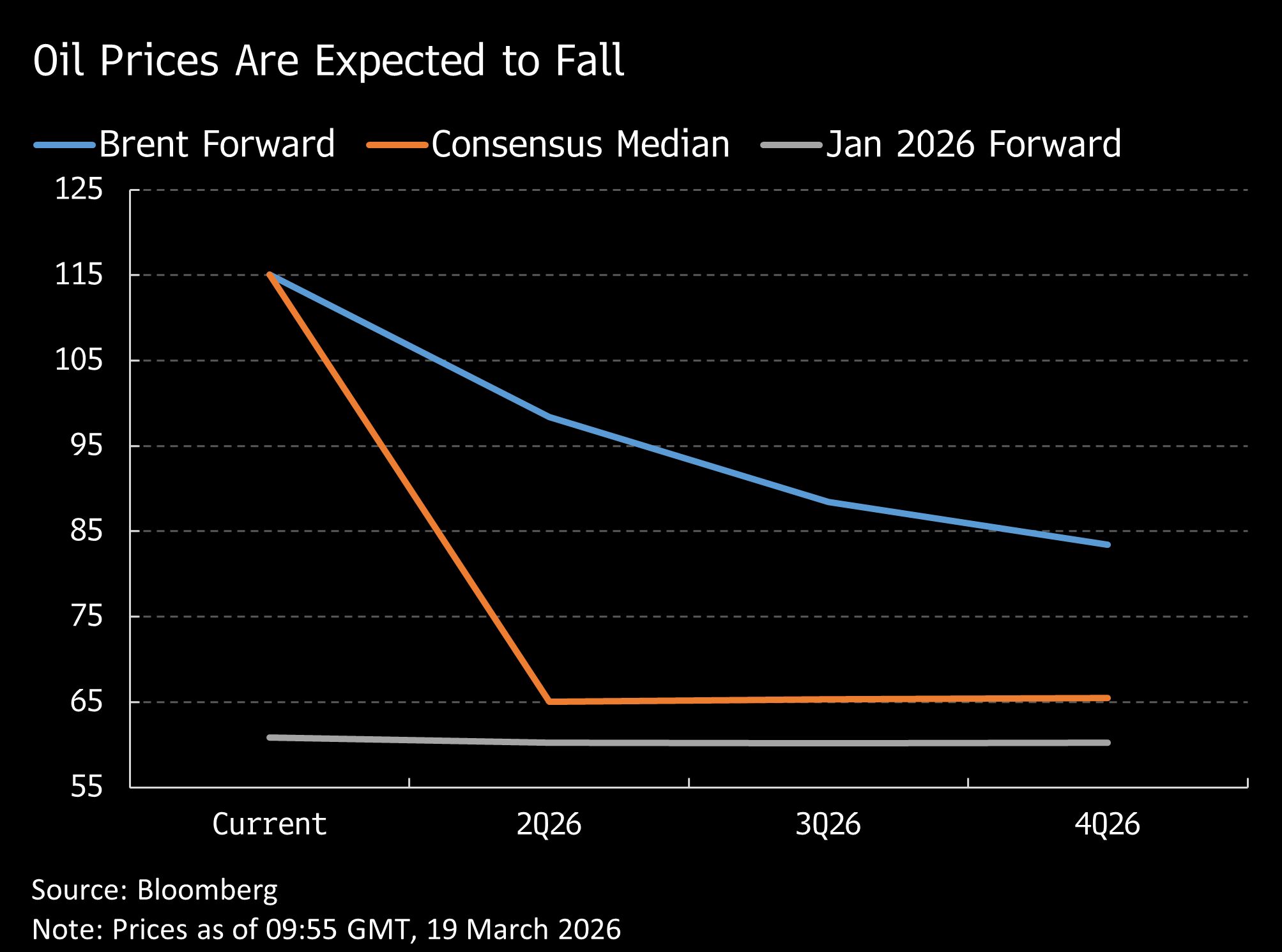

Markets appear reluctant to fully price the negative implications of higher energy prices. Perhaps commodity investors are more pessimistic about geopolitical risks than those in financial assets, as Simon White has noted.

Saying that, despite sentiment having weakened in recent days as energy infrastructure has been targeted, forward curves continue to reflect expectations of lower energy prices ahead.

That creates a clear tension. Either commodity prices fall, validating current pricing, or the macro impact begins to show in the data.

In the latter case, both bonds and equities remain vulnerable, whether through a sharp repricing on adverse headlines or a more gradual adjustment as expectations shift.

© 2026 Bloomberg