December 22, 2024

Input your search keywords and press Enter.

Pay TV operator MultiChoice has lost 1.1 million DStv subscribers across its Premium, Compact Plus, Compact and Commercial (hotel/restaurant/tavern) customers over the last four years.

The September 2020 base was heavily impacted – positively – by the Covid-19 pandemic and was almost certainly the peak for pay TV in the country. Those numbers will not be reached again, particularly in the Premium and mid-market segments.

The upper end of the market, which it terms its Premium segment (which includes the Premium and Compact Plus bouquets), has declined by more than 21% over those four years.

However, most of the decline has come in its mid-market segment, primarily the DStv Compact subscriber base. It adds commercial customers into this segment (like it does with Compact Plus in the ‘Premium’ one) so that it doesn’t have to disclose the movements in the specific DStv Premium and DStv Compact bases.

This is based on the number of subscribers who were active at any point in the last 90 days of each half-year (between July and September).

Counter-intuitively, the group has focused on its 90-day active subscriber base in recent years versus the actual number of subscribers on 30 September, as this tends to give a better view of trends over time.

This year, though, it reverted to highlighting the latter (presumably as it painted a better picture).

| 90-day active subscribers | Sep 2020 | Sep 2021 | Sep 2022 | Sep 2023 | Sep 2024 |

| Premium segment (Premium, Compact Plus) | 1.4m | 1.4m | 1.3m | 1.3m | 1.1m |

| Mid-market segment (Compact, Commercial) | 2.9m | 2.8m | 2.7m | 2.3m | 2.1m |

It cites research from Eighty20 showing that income in the middle-income market (R15 000 to R25 000 per month) declined in real terms by 10% between the end of 2022 and the middle of 2024.

At the same time, instalments as a percentage of net income are up 9% to 79%, leaving limited discretionary spend available each month (despite no load shedding).

It highlights that the decline of its Premium bouquet base is “slowing” with a drop of 2% over the last year, versus 6% a year in the two prior years.

Overall, it lost half a million subscribers (based on the 90-day active definition) over the last year. It now has 8.1 million, down from 8.6 million in 2023 – a 6% drop. There have been declines across all three segments (premium, mid-market, and mass market).

Rest of Africa looks even worse

The picture in the rest of Africa looks even worse, with a 14% decline in the past year – a loss of nearly two million subscribers (to 11.2 million). Here, the declines are particularly pronounced in the premium and mass-market bases.

The biggest percentage decline was in Zambia (-60%), but in absolute subscriber terms, the 18% drop in Nigeria is the largest.

In the current market, it has limited pricing power to offset the declines.

It increased prices by, on average, 5.9% in South Africa and 17% in other countries. Inflation in most of these key markets is running at 30%-plus. In South Africa, the lowest increases were in that battling mid-market base (read: DStv Compact).

Additional services

It continues to bang the drum of adding additional services to offset the decline in subscriber revenue, which is remarkably at odds with major shareholder and suitor Canal+’s stated strategy. This includes Showmax 2.0, DStv Internet, its betting platform KingMakers and its decoder insurance business.

This has helped it eke out an increase in the average revenue per user (ARPU) of 3% in South Africa to R289 a month. Only problem? It is selling the rump of its insurance business, with R600 million in revenue in the six months, to Sanlam.

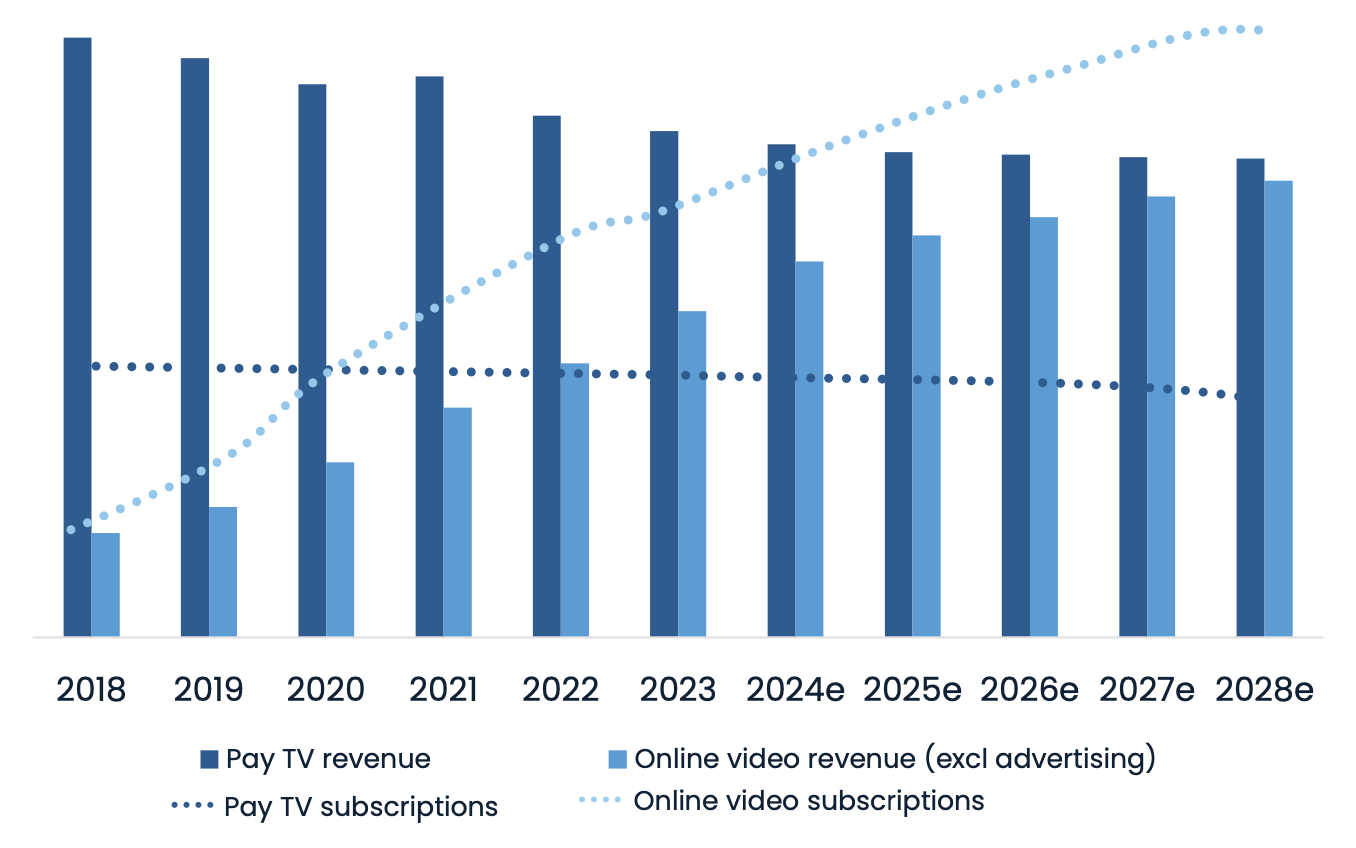

It admits that pay TV growth has “plateaued” globally, although subscriptions are in structural decline and revenue is dropping quicker.

Source: Omdia (Oct 2024) via MultiChoice

The streaming opportunity, primarily via Showmax 2.0, is central to its strategy going forward. It says the paying Showmax subscriber base is up 50% year-on-year, driven by the 30% increase since its relaunch in February. Revenue from DStv Stream (the standalone offering not requiring a decoder) is up 71% year-on-year.

It continues to cut costs aggressively across the group, with a target of R2.5 billion for the year to end-March (from R1.9 billion last FY). It has increased this from the R2 billion level it communicated six months ago.

To put this in perspective, the R1.33 billion in costs taken out of the business in the first six months was higher than the R1.28 billion in cost savings from the whole of the 2023 financial year.