July 25, 2024

Input your search keywords and press Enter.

IT is a year of many elections worldwide, and frustratingly, we’ll have to wait right to the end for the most consequential and possibly closest run of the lot. Six months from now, the US will go to the polls to choose its president, congressional representatives, and state and local officials.

As things stand, it looks like the presidential election will be a rerun of the 2020 contest between Joe Biden (81) and Donald Trump (77), except that this time Trump is the challenger and Biden the incumbent. Biden, the presumptive Democratic candidate, is a lifelong politician. Trump, the likely Republican candidate, is a disruptor in politics, having built his career in real estate and entertainment. People either love him or hate him.

Biden is already the oldest US president ever. If Trump wins, he will narrowly be the second oldest, behind Biden. The median age in the US is 38, while life expectancy at birth for men is only 76.

Divided States of America

There are deep divisions in the US on key socio-cultural issues around race, gender, reproductive rights, immigration, gun rights and more. As the election nears, the noise around these ‘culture wars’ will only increase. For investors, however, economic policy matters the most.

Closer to the time, we will revisit the state of the US economy and what that means for the election prospects of the incumbent and the challenger. Notably, consumer confidence is remarkably low, given how strong the US economy is, especially compared to other developed countries. For this note, however, the focus is on what each candidate means for global markets.

There is some overlap between the economic policies of Trump and Biden. Both are wary of China, and both want to re-energise American manufacturing.

Biden, for instance, kept most of the import tariffs Trump imposed on China in 2018.

Under the CHIPS [‘Creating Helpful Incentives to Produce Semiconductors’] Act and the Inflation Reduction Act, the Biden administration has pumped billions into supporting US manufacturing of high-tech semiconductors, batteries and other green technologies. This has resulted in an almost three-fold increase in spending on the construction of manufacturing facilities.

US construction spending on factories. Source: LSEG Datastream

But there are also major differences. If Biden wins, we should expect broad policy continuity with his first term, including further investment in domestic manufacturing and infrastructure and an emphasis on green energy. He will respect the independence of key US domestic institutions, notably the Federal Reserve.

In the foreign policy terrain, he will continue to be engaged with Nato and back Ukraine’s fight against Russia. Though supportive of Israel’s war on Hamas, he has increasingly voiced his frustration at how it is conducted, and his ongoing backing cannot be taken for granted.

In a nutshell, a Biden win would probably not have many new investment implications. The same cannot be said for a second Trump presidency.

Before discussing this, an important caveat: It matters greatly who controls the two houses of Congress. Currently, the Democrats control the Senate, thanks only to the vice president’s ability to cast tie-breaking votes. The Republicans have a majority in the House of Representatives.

Major domestic policy changes, particularly regarding spending and taxation decisions, need congressional approval. In other words, if there is split control between the White House and the two chambers of Congress, the president cannot do much. If the same party sweeps the presidency and Congress, as Trump did in 2016 and Biden in 2020, there is room for action. In foreign policy, however, the president has more leeway to act unilaterally.

Fiscal fears

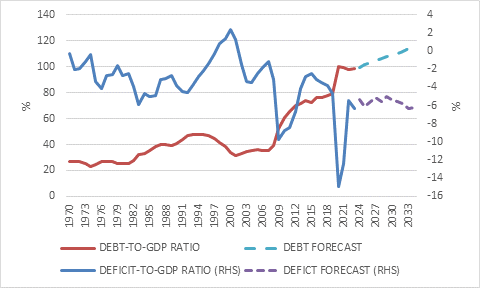

Irrespective of who wins, the US has a long-term fiscal problem. Its debt-to-GDP ratio of around 100% (depending on what is included) seemed sustainable when interest rates were at rock bottom before Covid. But at current levels, the US federal government will be spending around 4% of GDP on interest payments in the years ahead, according to the nonpartisan Congressional Budget Office’s predictions (this is close to the share of GDP South Africa currently spends).

Despite the solid economy, the US runs a 6% GDP deficit, usually associated with recessions (when tax revenues collapse and emergency spending rises). Worryingly, there is no sign that borrowing will be scaled back anytime soon. Neither candidate has shown any interest in addressing the seemingly inexorable rise in public debt.

Indeed, Trump will likely extend the 2017 tax cuts that favoured companies and wealthy individuals, which are set to expire at the end of 2025. If they are not extended, the tax burden on Americans will rise somewhat, which would be an economic headwind but reduce longer-term debt anxiety.

As noted, the future of fiscal policy depends greatly on which party controls Congress. Split White House-Congressional control also implies a recurrence of the debt ceiling stand-offs, government shutdowns and fiscal cliff scenarios that have dented trust in America’s fiscal policy process. The country really needs a sober and objective look at the mix of government debt, spending and taxation, but there is no indication of this happening.

US federal debt and deficit with projections. Source: Congressional Budget Office

Geopolitics

One of Trump’s first actions upon taking office was to pull out of the Paris Agreement on Climate Change. Biden rejoined in 2021, but Trump will likely withdraw the US from its global climate change commitments again. This would be disastrous since it is the world’s second-biggest carbon emitter behind China.

Also worrying, from the point of view of America’s allies, would be a scaling back on its outsized Nato commitments. Trump has criticised – probably correctly – large European countries like Germany, Italy and Spain for spending less than the targeted 2% of GDP on defence (annual US defence spending is around $850 billion, or 3.5% of GDP). He is very likely to halt US support for Ukraine, leaving it up to Europe to fund the fight against Russian aggression.

And while Trump is a China hawk when it comes to trade, he is probably less interested in going to war to defend Taiwan. In other words, from a geostrategic point of view, a Trump presidency will lead to a more divided West and an emboldened Russia and China.

You’re fired!

Trump appointed current Federal Reserve Chair Jerome Powell in 2018 but almost immediately had buyer’s regret. Powell raised interest rates, while Trump wanted lower rates to goose the stock market and support his political prospects. He made his feelings known on the matter, often venting on social media that the Fed had to cut rates. Not since Lyndon Johnson attacked William McChesney Martin at his Texas ranch in 1965 did a Fed chair face such direct and sustained pressure from a president.

More recently, Trump also attacked Powell for cutting rates ahead of this year’s election, which might help Biden a bit. Of course, the Fed has not done anything yet and, if anything, expectations for rate cuts have faded.

The last thing the Fed wants to do is seem politically motivated, but Trump appears to have already made up his mind that it is. He has said he will not renew Powell’s four-year term when it expires in 2026.

The two vice chairs’ terms expire in 2027.

The global trend over the past 30-odd years has been to give central banks complete independence to set monetary policy to avoid them becoming involved in election battles, changing interest rates for political reasons rather than in service of long-term macroeconomic stability. Perhaps it was naïve all along that this independence would last and a mistake to grant such an important policy area to unelected officials. However, a reduction in central bank independence and politicisation of monetary policy in the US would greatly undermine global bond market pricing and functioning.

Assuming Powell and his deputies serve their full terms, they can shield the Fed from political interference for the first half of Trump’s administration. Thereafter, it is anyone’s guess.

Fortunately, the FOMC, the committee that makes interest rate decisions, also has five rotating members from the presidents of the 12 regional Fed banks. These officials are not chosen by the US president but rather by the private sector boards of directors of the individual banks. In other words, it will probably require more than one Trump term (and he can’t serve another after 2028) to completely erode the Fed’s independence on monetary policy matters, but that doesn’t mean he won’t try.

Building walls

Immigration was one of Trump’s signature campaign issues back in 2016, though he never built the promised wall on the Mexican border. If anything, it is an even bigger issue today, with millions of migrants pouring over the southern border since the end of the pandemic.

Few issues raise the political temperature as much as immigration, particularly when the migrants are from poorer countries. That is true in the US as much as in South Africa. The difference is that the US is desperately short of workers.

The native-born workforce is shrinking. The post-Covid surge in migration has, therefore, eased this labour shortage somewhat, reducing upward pressure on wages that would otherwise have left the Fed extremely concerned that the economy was overheating and a wage-price spiral was underway.

While Trump is unlikely to deport millions of migrants as threatened, anything that constrains the supply of workers is likely to raise costs for businesses and consumers.

Tariff Man

An enduring legacy of Trump’s first term is protectionism, which is very much back on the agenda, not just in the US. The disruptions of the pandemic and Russia’s invasion of Ukraine have convinced many leaders that it is important to protect key domestic industries and build resilience in supply chains.

Reliance on China as a source of cheap production is now seen more as a liability than an asset, and China itself as more of a competitor than a partner.

Trump has promised another big increase in import tariffs on China but has also indicated that he will go further, imposing an across-the-board levy on all imports. Much like the mercantilists of the 17th and 18th centuries, he sees imports as a sign of weakness while exports signal strength. However, the US’s appetite for imports – and its large trade deficit – is also a sign of strong consumer demand. US factories cannot meet all this demand, definitely not at the price points US consumers are used to. Meanwhile, China’s export prowess is in part due to suppressed domestic demand.

Even if production shifts away from China, only the manufacturing of particularly high-value items will return to the US. Low-value manufacturing will still be done in low-cost countries within the US orbit. Since Trump renegotiated the North American Free Trade Agreement and replaced it with the USMCA (US-Mexico-Canada Agreement; apparently, the US had to be first in the name), Mexico seems safe as a beneficiary of this ‘friendshoring’ trend. We’ll have to see if other winners like Bangladesh and Vietnam can continue to fly under the radar.

Share of US imports by destination. Source: LSEG Datastream

Notably, despite dire predictions of the future of global trade, it hasn’t collapsed and, in fact, seems to be recovering in recent months. This is largely due to a cyclical improvement in global manufacturing.

Longer term, the risk remains that the global system fragments into trading blocs centred on China and the US. This will not only put upward pressure on the cost of manufactured goods but also make it more difficult for poorer countries to trade their way to prosperity, as Korea, Taiwan, and China have.

Trumpflation implications

Looking at the above, a Trump presidency will likely be inflationary. The combination of restricted labour supply, higher import tariffs, loose fiscal policy, and a central bank that loses credibility is a recipe for higher inflation. This suggests avoiding long-term US government bonds.

What about the dollar? On the one hand, a weakening of US policy institutions and the rule of law against the backdrop of the long-term debt problem should be dollar-negative. Uniquely among American presidents, Trump explicitly favours a weaker dollar to support exports and curb imports.

On the other hand, the dollar tends to rally in times of anxiety, and perhaps not even a Trump presidency is chaotic enough to offset the Pavlovian flight to the safety of the dollar. There is still no credible global alternative to the greenback. Whatever problems the US has, other major countries are in worse shape. The remaining triple-A countries, like Switzerland and Australia, are simply too small to replace the dollar.

In terms of equities, the US market outperformed the rest of the world in Trump’s first term, enjoying a boost from lower tax cuts and a rapid recovery from the Covid crash. But the Obama and Biden presidencies also saw US outperformance, as was the case during the Clinton-era internet boom (1992 to 2000).

The US lagged behind the rest of the world during George W Bush’s years (2000 to 2008), not due to his misadventures in Afghanistan and Iraq but rather the booming global economy, commodity supercycle, and weak dollar. Bush was also unlucky that the start and end of his presidency coincided with two massive bear markets. In contrast, the implosion of the Japanese bubble meant that his father’s one term saw the best US outperformance of non-US markets.

US vs non-US equities over presidential terms, US$. Source: LSEG Datastream

The one thing investors should not do is let their own political views get in the way of investment decisions. When Barack Obama was elected, there was a widespread view that he was a closet socialist who would tank the market – his eight years in office turned out to be great for the S&P 500. There were similar misgivings about Trump before his surprise victory in 2016, and those misgivings were similarly wrong.

Ultimately, there is too much uncertainty over who will win in November and what that winner ends up doing to make specific election-related portfolio changes other than being prepared for a range of outcomes. Nonetheless, while US politics has in the past mattered much less to market performance than generally believed, times are changing, and we need to pay attention.

Izak Odendaal is an investment strategist at Old Mutual Wealth.